Energy security tops political agendas as prospects for offshore wind recovery gain momentum, TGS | 4C report finds

OSLO, Norway (15 June 2026) — Offshore wind market indicators remained subdued during the second quarter of 2026, while renewed focus on energy security is raising prospects for the industry’s recovery.

Released today, the latest quarterly Global Market Overview report from wind market intelligence house TGS | 4C notes that UK, France and Germany are among the countries that have accelerated renewable energy ambitions in attempts to lower reliance on imported energy.

The latest outlook shows slightly lowered 2030 forecasts and moderately raised 2040 expectations for offshore wind, reflecting short-term delivery challenges but stronger long-term fundamentals. At the same time, the report notes that market conditions for offshore wind are improving on several fronts, supporting more consistent progression in 2026 and beyond.

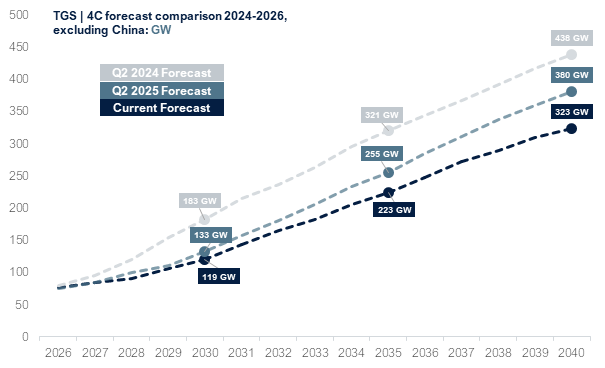

The global offshore wind forecast for installed capacity in 2030 has been reduced by 11% year on year, with expected capacity outside China declining from 133 GW to 119 GW. Forecasts for 2030 have reduced by 2 GW since last quarter, primarily reflecting continued auction and project timing delays.

This analysis finds a 15% drop in 2040 expectations from Q2 2025 and a 26% drop from expectations in Q2 2024, highlighting the scale of recent market recalibration. 2026 shows signs of improvement, with many projects progressing to later stages of the pipeline, suggesting a large buildout through the next decade.

Q2 2026 key indicators:

- Auctions: No Q2 auctions have been awarded. AO9 in France (Site + offtake) has been delayed, and Saare 3 (Site) in Estonia failed. On a positive note, Denmark (Site + offtake) and South Korea (Offtake) have confirmed that they have received more bidders than necessary for the auction to award, despite not awarding in this quarter.

- Commissioning: Q2 has seen 518 MW coming online outside China, and 1.1 GW inside China. This figure is expected to increase to around 15 GW by the end of the year, making it the second highest year on record. Global operational capacity is now at 91.5 GW.

- Permitting: Three projects, all in the UK, secured consent in Q2 2026: the 2×1.5 GW Dogger Bank South and North Falls (504 MW). TGS | 4C forecasts 20 GW of projects consented in 2026, led by Europe with 18.6 GW.

- Investment: 518 MW of FID (Final Investment Decisions) were made in Q2, entirely in APAC: 390 MW in South Korea and 128 MW in Vietnam. The full-year 2026 FID forecast stands at 8.8 GW, reflecting the accumulated backlog of projects delayed through the 2022–2024 cycle.

- The effects of the closure of the Strait of Hormuz have been realised in diesel prices, with a 34.6% YoY price increase. Hot-rolled coil (HRC) steel is also up 37% YoY, and copper is up 35% YoY. Geopolitical events, such as the Strait of Hormuz or tariffs in the US, are playing a significant role in offshore wind at present, adding risk and inflationary pressure.

“Q2 has been slow and stable but preceded an active first half of the year, with highlights that include the UK’s first Allocation Round 7 projects pushing forward to FID and Allocation Round 8 awarding a healthy stream of new contracts,” noted Jordan May, Senior Analyst at TGS | 4C. “There are nine ongoing auctions and another fifteen due to start before the end of the year. The industry is rife with global activity, but in strained market conditions, determining bankability is harder than ever.”

“The uncertainty caused by the war in Iran and the ensuing issues in the Strait of Hormuz has pushed energy security to the top of political agendas. The impact on key offshore wind indicators is not yet showing in the short term, but the industry can look forward to political boosts in key markets going forward,” said Ivar Slengesol, Managing Director and VP, TGS | 4C.

This edition includes a biannual floating report, which shows a reduced floating outlook, an updated floating attractiveness framework, and an updated outlook on future foundation types. TGS | 4C expects that by 2030, 3.1 GW of floating wind will begin installation activities. By another measure, 253 turbines will be installed. 4C expects that the turbine power in 2030 will be around 17 MW. The UK remains the world’s most attractive floating wind market, followed by France and Japan, according to the updated Floating Wind Market Attractiveness Index.

The findings highlight a growing divide between the most and least attractive countries due to various market-specific factors.

The Quarterly Market Overview Report is available exclusively to TGS | 4C subscribers, providing decision-ready forecasts, regional analysis and insights into policy, auctions and project pipelines across global offshore wind markets. This edition includes a deep dive into foundation concepts to support technology and investment decisions.

TGS | 4C provides intelligence reports on offshore energy trends via its 4C Intelligence platform. As a division of TGS, a leading energy data and intelligence provider, it also offers consultancy services for offshore projects, including offshore wind, subsea power cables, telecommunications, pipelines, and geospatial IT and GIS services. For further information, please visit www.tgs4c.com (https://www.tgs4c.com/).

Offshore wind capacity forecasts to 2040, illustrating successive revisions based on analysis from TGS | 4C.

About TGS

TGS provides advanced data and intelligence to companies active in the energy sector. With leading-edge technology and solutions spanning the entire energy value chain, TGS offers a comprehensive range of insights to help clients make better decisions. Our broad range of products and advanced data technologies, coupled with a global, extensive and diverse energy data library, make TGS a trusted partner in supporting the exploration and production of energy resources worldwide. For further information, please visit www.tgs.com (https://www.tgs.com/).

For media inquiries, contact:

Bård Stenberg

IR & Business Intelligence

investor@tgs.com

![]()