Enlight Renewable Energy Reports Third Quarter 2025 Financial Results

All of the amounts disclosed in this press release are in U.S. dollars unless otherwise noted

TEL AVIV, Israel, Nov. 12, 2025 (GLOBE NEWSWIRE) — Enlight Renewable Energy (NASDAQ: ENLT, TASE: ENLT) today reported financial results for the third quarter of 2025 ending September 30, 2025. Registration links for the Company’s earnings English and Hebrew conference call and webcasts can be found at the end of this earnings release.

| The entire suite of the Company’s 3Q25 financial results can be found on our IR website at https://enlightenergy.co.il/data/financial-reports/ | ||

Financial Highlights

9 months ending September 30, 2025

- Revenue and income of $430m, up 46% year over year

- Net income of $140m, up 140% year over year

- Adjusted EBITDA1 of $339m, up 52% year over year

- Cash flow from operations of $162m, up 3% year over year

3 months ending September 30, 2025

- Revenues and income of $165m, up 46% year over year

- Net Income of $32m, up 33% year over year

- Adjusted EBITDA1 of $112m, up 23% year over year

- Cash flow from operations of $71m, up 7% year over year

________________________

1 The Company is unable to provide a reconciliation of Adjusted EBITDA to Net Income on a forward-looking basis without unreasonable effort because items that impact this IFRS financial measure are not within the Company’s control and/or cannot be reasonably predicted. Please refer to the reconciliation table in Appendix 2.

Summary of key financial results for 3Q25 and 9M25

| For the three months ended | For the nine months ended | |||||

| ($ millions) | 30/09/2025 | 30/09/2024 | % change | 30/09/2025 | 30/09/2024 | % change |

| Revenues and Income | 165 | 113 | 46% | 430 | 295 | 46% |

| Net Income | 32 | 24 | 33% | 140 | 58 | 140% |

| Adjusted EBITDA | 112 | 91 | 23% | 339 | 224 | 52% |

| Cash Flow from Operating Activities | 71 | 66 | 7% | 162 | 158 | 3% |

Raising full-year guidance ranges

- On the back of strong 9M25 results, we are increasing full year 2025 guidance ranges. Revenue guidance rises to $555-565m from $520-535m previously, and Adjusted EBITDA guidance rises to $405-415m from $385-400m previously. This represents a 6.0% and 4.5% increase at the midpoint for both metrics, respectively. The increase in guidance and the narrowing of the range reflect our confidence in the continued robust growth across all parts of our business.

- A detailed analysis of financial results appears below.

Adi Leviatan, CEO of Enlight Renewable Energy: “The third quarter financial results reflect impressive achievements above our expectations, underscoring the Company’s strength, the dedication of team, and our focused business strategy. Enlight is well positioned for continued accelerated global growth, capitalizing on opportunities in the renewable energy market, which continues to benefit from favorable fundamentals. We will continue to operate with innovation and responsibility to develop the clean energy sector and strengthen our position as a leading player in the global energy market.”

Portfolio Review

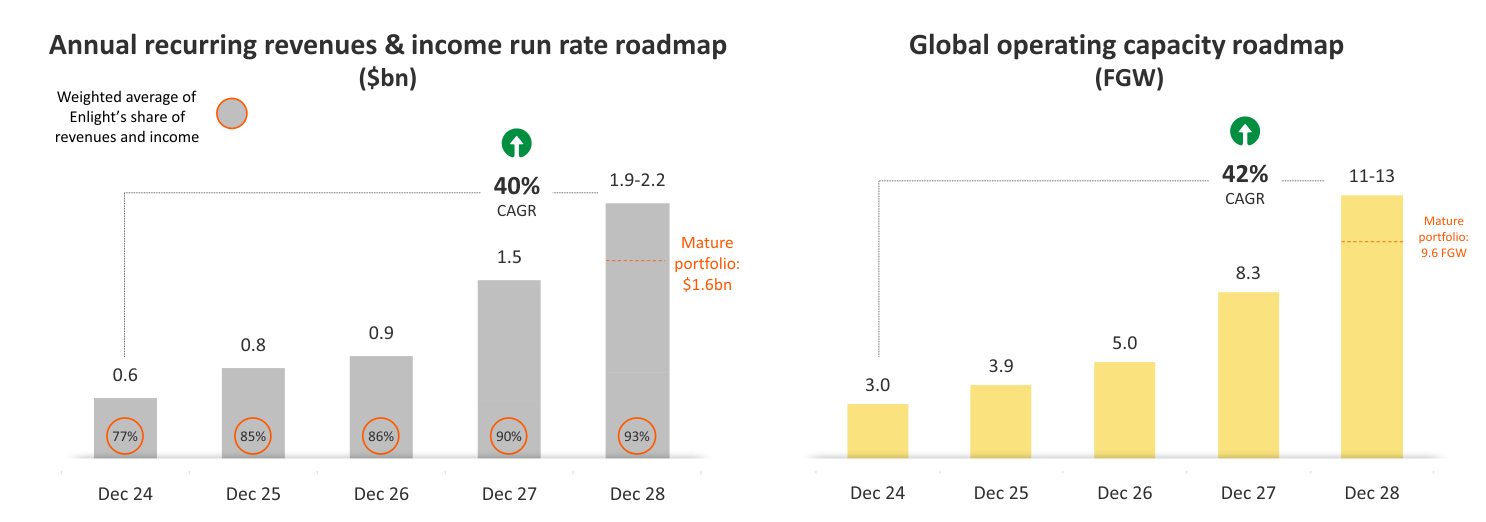

This quarter we continued to expand our portfolio and advance our projects through the various phases of development. Enlight’s total portfolio is comprised of 20.4 GW of generation capacity and 58.1 GWh energy storage (totaling 37.0 FGW2), an increase of 23% from the total portfolio of 30.2 FGW at the end of 2024. Of this, the Mature portfolio component (including operating projects, projects under construction or in pre-construction) contains 6.2 GW generation capacity and 11.8 GWh of storage (9.6 FGW in total), an increase of 12% from the Mature portfolio of 8.6 FGW at the end of 2024.

Enlight has achieved safe harbor status for its entire U.S. Mature portfolio (5.6 FGW), as well as for an additional 3.3 FGW of projects in its Advanced Development and Development portfolios. An additional 5-8 FGW of projects are expected to achieve safe harbor status by July 2026, of which 2-4 FGW are expected to be safe harbored by the end of this year.

The composition of Enlight’s portfolio appears in the following table:

| Component | Status | FGW3 | Annual revenues & income run rate4($m) | ||

| Operating | Commercial operation | 3.1 | ~560 | ||

| Under Construction | Under construction | 2.9 | ~550 | ||

| Pre-Construction | 0-12 months to start of construction | 3.6 | ~500 | ||

| Total Mature Portfolio | Mature | 9.6 | ~$1,610m | ||

| Advanced Development | 13-24 months to start of construction | 6.1 | – | ||

| Development | 2+ years to start of construction | 21.3 | – | ||

| Total Portfolio | 37.0 | – | |||

________________________

2 FGW (Factored GW) is a consolidated metric combining generation and storage capacity into a uniform figure based on the ratio of construction costs. The company’s current weighted average construction cost ratio is 3.5 GWh of storage per 1 GW of generation: FGW = GW + GWh / 3.5

3 FGW (Factored GW) is a consolidated metric combining generation and storage capacity into a uniform figure based on the ratio of construction costs. The company’s current weighted average construction cost ratio is 3.5 GWh of storage per 1 GW of generation: FGW = GW + GWh / 3.5

4 As of as of November 11, 2025 (“the Approval Date”).

- Operating component of the portfolio: 3.1 FGW

- The operational portfolio generates annualized revenues and income run rate of approximately $560m.

- The operational portfolio generates annualized revenues and income run rate of approximately $560m.

- Under Construction component of the portfolio: 2.9 FGW

- Contains four major projects in the U.S. with a total capacity of 2.5 FGW.

- Of these, projects Roadrunner and Quail Ranch are expected to reach COD by the end of 2025. Roadrunner has already begun testing and electrification procedures.

- Projects under construction are expected to contribute ~$550m to the annual revenues and income run rate during their first full year of operation.

- Pre-construction component of the portfolio: 3.6 FGW

- Three significant additions were made to this component of the portfolio during the quarter:

- Bertikow, a 246 FMW stand-alone storage project acquired in Germany, marking the Company’s first project in this country.

- Edison, a 59 FMW stand-alone storage project acquired in Poland.

- Neot Smadar, a 184 FMW stand-alone storage project located in Israel.

- Pre-construction projects are expected to contribute ~$500 in revenues and income in their first full year of operations.

- Project CO-Bar (1.4 FGW) has obtained an LGIA and is waiting for approvals before execution and construction.

- Pre-construction projects are expected to contribute ~$500m to the annual revenues and income run rate during their first full year of operation.

- Three significant additions were made to this component of the portfolio during the quarter:

With the completion of the current Mature portfolio’s pre-construction and under construction projects, Enlight’s operating capacity is expected to rise to 9.6 FGW and to generate an annualized revenue and income run rate of $1.6bn by the end of 2028.

- Advanced Development component of the portfolio component: 6.1 FGW

- 5.1 FGW in the U.S., with 100% of the capacity having passed completion of the System Impact Study. The advanced development portfolio also includes 0.7 FGW in Europe and 0.3 FGW in MENA.

- Development component of the portfolio: 21.3 FGW

- 14.6 FGW in the U.S. with broad geographic presence, including the PJM, WECC, SPP and MISO regions. The development portfolio also includes 2.7 FGW in Europe and 4.0 FGW in MENA.

Roadmap to Revenues and Income Run-Rate of ~$2.0bn by the end of 20285

________________________

5 Expected Adjusted EBITDA margin of approximately 70%-80% (including tax benefits) for the years shown. FGW (Factored GW) is a consolidated metric combining generation and storage capacity into a uniform figure based on the ratio of construction costs. The company’s current weighted average construction cost ratio is 3.5 GWh of storage per 1 GW of generation: FGW = GW + GWh / 3.5. The expected growth in 2028 encompasses the Company’s operations in all geographies. Expected growth relies on business plans which rely on development conditions and assumptions regarding electricity prices, and are contingent on current trends known to the Company at this time. 4 The company’s revenues from tax benefits are estimated at approximately 19-23% of the total revenues & income run rate for December 2025; approximately 24-28% of the total revenue run rate for December 2026, and approximately 28-33% of the total revenues & income run rate for December 2027 and December 2028.

Project and Corporate Finance

- During the quarter, the Company secured project finance from multiple sources to support our U.S. expansion plans:

- Financial close totaling approximately $1.4bn of loans for the Snowflake A project (1.1 FGW), the largest in the Company’s history. Snowflake A is expected to reach COD by 2H27, and generate revenues and income of $223-229m and EBITDA of $199-204m in its first full year of operation.

- Tax equity financing for the Roadrunner and Quail Ranch projects (0.8 FGW combined) totaling approximately $470m. Both projects are expected to reach COD by the end of this year, and together generate revenues and income of $143-147m and EBITDA of $124-127m in their first full year of operation.

- Completion of a $350m mezzanine loan with competitive margins of 2.7% – 3.2% above SOFR and flexible drawdown and repayment terms, supporting the development and operational needs of projects now under construction in the U.S.

- Raising approximately $300m in share equity through a private placement to Israeli institutional investors.

- Cash and cash equivalents at the “topco” level6 were $387m as at the balance sheet date.

- As at the balance sheet date, the Company maintained $525m of credit facilities, of which $109m have been drawn. In addition, we have approximately $1.4bn of LC and surety bond facilities supporting our global expansion, of which $590m has been drawn at end of the quarter.

2025 Guidance

Construction and commissioning

- We expect commissioning of Roadrunner and Quail Ranch, with a combined capacity of 0.8 FGW, toward the end of 2025.

Raising financial guidance ranges

- Total revenues and income7 for 2025 are now expected to range between $555m and $565m, up 6.0% at the midpoint from the previous range of $520m to $535m.

- Adjusted EBITDA8 for 2025 is expected to range between $405m and $415m, up 4.5% at the midpoint from the previous range of $385m to $400m.

- Approximately 90% of the electricity volumes expected to be generated in 2025 will be sold at fixed prices through PPAs or hedges.

________________________

6 Including Enlight Renewable Energy, headquarter companies in Europe and the U.S. and Clenera, and excluding other subsidiaries and project-linked entities.

7 Total revenues and income include revenues from the sale of electricity along with income from tax benefits from US projects amounting to $80m-$90m.

8 EBITDA is a non-IFRS financial measure. The Company is unable to provide a reconciliation of EBITDA to Net Income on a forward-looking basis without unreasonable effort because items that impact this IFRS financial measure are not within the Company’s control and/or cannot be reasonably predicted. Please refer to the reconciliation table in Appendix 2.

Financial Results Analysis

| Revenues & Income by Segment | |||||||

| ($ millions) | For the three months ended | For the nine months ended | |||||

| Segment | 30/09/2025 | 30/09/2024 | % change | 30/09/2025 | 30/09/2024 | % change | |

| MENA | 78 | 55 | 40% | 173 | 122 | 42% | |

| Europe | 45 | 46 | (2%) | 145 | 147 | (2%) | |

| U.S. | 42 | 9 | 379% | 111 | 19 | 493% | |

| Other | 0 | 3 | (92%) | 1 | 7 | (82%) | |

| Total Revenues & Income | 165 | 113 | 46% | 430 | 295 | 46% | |

Revenues & Income

In the third quarter of 2025, the Company’s total revenues and income increased to $165m, up from $113m last year, a growth rate of 46% year over year. This was composed of revenues from the sale of electricity, which rose 27% to $139m compared to $109m in the same period of 2024, as well as recognition of $27m in income from tax benefits compared to $4m in 3Q24.

The Company benefited from the revenues and income contribution of newly operational projects. In the past 12 months 106 MW and 1,435 MWh of new projects were connected to the grid and began selling electricity, including Atrisco in the U.S, various projects in Israel, Pupin in Serbia, and Tapolca in Hungary. The most notable increases in revenue from the sale of electricity originated at Atrisco, which added $11m, followed by Israeli projects with $7m, while Pupin contributed $4m. In total, new projects contributed $22m to revenues from the sale of electricity. Recognition of tax benefit income increased by $23m due to the initial commissioning of Atrisco. Revenues and income for the quarter were distributed between MENA (27%), Europe (47%), and the US (26%).

Net Income

In the third quarter of 2025, the Company reported net income of $32m, representing a 33% increase from $24m in the same period last year. New projects contributed $12m to net income, while the refinancing of the Gecama wind project added an additional $10m to net income. This was offset by a $5m rise in operating expenses and a decline of $7m other income, all after tax.

Adjusted EBITDA9

The Company’s Adjusted EBITDA grew by 23% to $112m in the third quarter of 2025, compared to $91m for the same period in 2024. Growth in revenues and income contributed $52m. This was offset by an increase of $17m in COGS linked to the addition of new projects, and an increase of $7m in G&A expenses. During the quarter, the Company recognized $3m in compensation linked to turbine failures at the Björnberget project in Sweden, compared the recognition of $10m in compensation at the same project during 3Q24.

________________________

9 The Company is unable to provide a reconciliation of Adjusted EBITDA to Net Income on a forward-looking basis without unreasonable effort because items that impact this IFRS financial measure are not within the Company’s control and/or cannot be reasonably predicted. Please refer to the reconciliation table in Appendix 2.

Conference Call Information

Enlight plans to hold its Third Quarter 2025 Conference Call and Webcasts on Wednesday, November 12, 2025 to review its financial results and business outlook in both English and Hebrew. Management will deliver prepared remarks followed by a question-and-answer session. Participants can join by dial-in or webcast:

- English Conference Call at 8:00am ET / 3:00pm Israel:Please pre-register to join by conference call using the following link:

https://register-conf.media-server.com/register/BIc02636ac75af4b9b962a688d1f9e8115

Upon registering, you will be emailed a dial-in number, direct passcode and unique PIN.

- English Webcast at 8:00am ET / 3:00pm Israel:

Please register and join by webcast at the following link: - Hebrew Webcast at 6:00am ET / 1:00pm Israel:

Please join the webcast at the following link:https://enlightenergy-co-il.zoom.us/webinar/register/WN__wcPWrTGTXyuXG6P-eO3dw

The press release with the financial results as well as the investor presentation materials will be accessible from the Company’s website prior to the conference call. An archived version of the webcast will be available on the Company’s investor relations website at https://enlightenergy.co.il/info/investors/.

Supplemental Financial and Other Information

We intend to announce material information to the public through the Enlight investor relations website at https://enlightenergy.co.il/info/investors, SEC filings, press releases, public conference calls, and public webcasts. We use these channels to communicate with our investors, customers, and the public about our company, our offerings, and other issues. As such, we encourage investors, the media, and others to follow the channels listed above, and to review the information disclosed through such channels. Any updates to the list of disclosure channels through which we will announce information will be posted on the investor relations page of our website.

Non-IFRS Financial Measures

This release presents Adjusted EBITDA, a financial metric, which is provided as a complement to the results provided in accordance with the International Financial Reporting Standards as issued by the International Accounting Standards Board (“IFRS”). A reconciliation of the non-IFRS financial information to the most directly comparable IFRS financial measure is provided in the accompanying tables found at the end of this release.

We define Adjusted EBITDA as net income (loss) plus depreciation and amortization, share based compensation, finance expenses, taxes on income and share in losses of equity accounted investees and minus finance income and non-recurring portions of other income, net. For the purposes of calculating Adjusted EBITDA, compensation for inadequate performance of goods and services procured by the Company are included in other income, net. Compensation for inadequate performance of goods and services reflects the profits the Company would have generated under regular operating conditions and is therefore included in Adjusted EBITDA. With respect to gains (losses) from asset disposals, as part of Enlight’s strategy to accelerate growth and reduce the need for equity financing, the Company sells parts of or the entirety of selected renewable project assets from time to time, and therefore includes realized gains or losses from these asset disposals in Adjusted EBITDA. In the case of partial assets disposals, Adjusted EBITDA includes only the actual consideration less the book value of the assets sold. Our management believes Adjusted EBITDA is indicative of operational performance and ongoing profitability and uses Adjusted EBITDA to evaluate the operating performance and for planning and forecasting purposes.

Non-IFRS financial measures have limitations as analytical tools and should not be considered in isolation or as substitutes for financial information presented under IFRS. There are a number of limitations related to the use of non-IFRS financial measures versus comparable financial measures determined under IFRS. For example, other companies in our industry may calculate the non-IFRS financial measures that we use differently or may use other measures to evaluate their performance. All of these limitations could reduce the usefulness of our non-IFRS financial measures as analytical tools. Investors are encouraged to review the related IFRS financial measure, Net Income, and the reconciliations of Adjusted EBITDA provided below to Net Income and to not rely on any single financial measure to evaluate our business.

Special Note Regarding Forward-Looking Statements

This press release contains forward-looking statements within the meaning of the U.S. Private Securities Litigation Reform Act of 1995. We intend such forward-looking statements to be covered by the safe harbor provisions for forward-looking statements as contained in Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. All statements contained in this press release other than statements of historical fact, including, without limitation, statements regarding the Company’s business strategy and plans, capabilities of the Company’s project portfolio and achievement of operational objectives, market opportunity, utility demand and potential growth, discussions with commercial counterparties and financing sources, pricing trends for materials, progress of Company projects, including anticipated timing of related approvals and project completion and anticipated production delays, the Company’s future financial results, expected impact from various regulatory developments and anticipated trade sanctions, expectations regarding wind production, electricity prices and windfall taxes, and Revenues and Income and Adjusted EBITDA guidance, the expected timing of completion of our ongoing projects, and the Company’s anticipated cash requirements and financing plans , are forward-looking statements. The words “may,” “might,” “will,” “could,” “would,” “should,” “expect,” “plan,” “anticipate,” “intend,” “target,” “seek,” “believe,” “estimate,” “predict,” “potential,” “continue,” “contemplate,” “possible,” “forecasts,” “aims” or the negative of these terms and similar expressions are intended to identify forward-looking statements, though not all forward-looking statements use these words or expressions.

These statements are neither promises nor guarantees, but involve known and unknown risks, uncertainties and other important factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements, including, but not limited to, the following: our ability to site suitable land for, and otherwise source, renewable energy projects and to successfully develop and convert them into Operational Projects; availability of, and access to, interconnection facilities and transmission systems; our ability to obtain and maintain governmental and other regulatory approvals and permits, including environmental approvals and permits; construction delays, operational delays and supply chain disruptions leading to increased cost of materials required for the construction of our projects, as well as cost overruns and delays related to disputes with contractors; disruptions in trade caused by political, social or economic instability in regions where our components and materials are made; our suppliers’ ability and willingness to perform both existing and future obligations; competition from traditional and renewable energy companies in developing renewable energy projects; potential slowed demand for renewable energy projects and our ability to enter into new offtake contracts on acceptable terms and prices as current offtake contracts expire; offtakers’ ability to terminate contracts or seek other remedies resulting from failure of our projects to meet development, operational or performance benchmarks; exposure to market prices in some of our offtake contracts; various technical and operational challenges leading to unplanned outages, reduced output, interconnection or termination issues; the dependence of our production and revenue on suitable meteorological and environmental conditions, and our ability to accurately predict such conditions; our ability to enforce warranties provided by our counterparties in the event that our projects do not perform as expected; government curtailment, energy price caps and other government actions that restrict or reduce the profitability of renewable energy production; electricity price volatility, unusual weather conditions (including the effects of climate change, could adversely affect wind and solar conditions), catastrophic weather-related or other damage to facilities, unscheduled generation outages, maintenance or repairs, unanticipated changes to availability due to higher demand, shortages, transportation problems or other developments, environmental incidents, or electric transmission system constraints and the possibility that we may not have adequate insurance to cover losses as a result of such hazards; our dependence on certain operational projects for a substantial portion of our cash flows; our ability to continue to grow our portfolio of projects through successful acquisitions; changes and advances in technology that impair or eliminate the competitive advantage of our projects or upsets the expectations underlying investments in our technologies; our ability to effectively anticipate and manage cost inflation, interest rate risk, currency exchange fluctuations and other macroeconomic conditions that impact our business; our ability to retain and attract key personnel; our ability to manage legal and regulatory compliance and litigation risk across our global corporate structure; our ability to protect our business from, and manage the impact of, cyber-attacks, disruptions and security incidents, as well as acts of terrorism or war; changes to existing renewable energy industry policies and regulations that present technical, regulatory and economic barriers to renewable energy projects; the reduction, elimination or expiration of government incentives or benefits for, or regulations mandating the use of, renewable energy; our ability to effectively manage the global expansion of the scale of our business operations; our ability to perform to expectations in our new line of business involving the construction of PV systems for municipalities in Israel; our ability to effectively manage our supply chain and comply with applicable regulations with respect to international trade relations, the impact of tariffs on the cost of construction and our ability to mitigate such impact, sanctions, export controls and anti-bribery and anti-corruption laws; our ability to effectively comply with Environmental Health and Safety and other laws and regulations and receive and maintain all necessary licenses, permits and authorizations; our performance of various obligations under the terms of our indebtedness (and the indebtedness of our subsidiaries that we guarantee) and our ability to continue to secure project financing on attractive terms for our projects; limitations on our management rights and operational flexibility due to our use of tax equity arrangements; potential claims and disagreements with partners, investors and other counterparties that could reduce our right to cash flows generated by our projects; our ability to comply with increasingly complex tax laws of various jurisdictions in which we currently operate as well as the tax laws in jurisdictions in which we intend to operate in the future; the unknown effect of the dual listing of our ordinary shares on the price of our ordinary shares; various risks related to our incorporation and location in Israel, including the ongoing war in Israel, where our headquarters and some of our wind energy and solar energy projects are located; the costs and requirements of being a public company, including the diversion of management’s attention with respect to such requirements; certain provisions in our Articles of Association and certain applicable regulations that may delay or prevent a change of control; and other risk factors set forth in the section titled “Risk factors” in our Annual Report on Form 20-F for the fiscal year ended December 31, 2024, filed with the Securities and Exchange Commission (the “SEC”), as may be updated in our other documents filed with or furnished to the SEC.

These statements reflect management’s current expectations regarding future events and operating performance and speak only as of the date of this press release. You should not put undue reliance on any forward-looking statements. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee that future results, levels of activity, performance and events and circumstances reflected in the forward-looking statements will be achieved or will occur. Except as required by applicable law, we undertake no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise, after the date on which the statements are made or to reflect the occurrence of unanticipated events.

About Enlight

Founded in 2008, Enlight develops, finances, constructs, owns, and operates utility-scale renewable energy projects. Enlight operates across the three largest renewable segments today: solar, wind and energy storage. A global platform, Enlight operates in the United States, Israel and 11 European countries. Enlight has been traded on the Tel Aviv Stock Exchange since 2010 (TASE: ENLT) and completed its U.S. IPO (Nasdaq: ENLT) in 2023.

Company Contacts

Limor Gruber

Director IR

investors@enlightenergy.co.il

Yonah Weisz

Director IR

investors@enlightenergy.co.il

Erica Mannion or Mike Funari

Sapphire Investor Relations, LLC

+1 617 542 6180

investors@enlightenergy.co.il

Appendix 1 – Financial information

| Consolidated Statements of Income | ||||||||

| For the nine months ended September 30 | For the three months ended September 30 | |||||||

| 2025 | 2024(*) | 2025 | 2024(*) | |||||

| USD in | USD in | USD in | USD in | |||||

| Thousands | Thousands | Thousands | Thousands | |||||

| Revenues | 364,411 | 284,590 | 138,536 | 109,495 | ||||

| Tax benefits | 65,493 | 10,102 | 26,521 | 3,576 | ||||

| Total revenues and income | 429,904 | 294,692 | 165,057 | 113,071 | ||||

| Cost of sales (**) | (95,839) | (54,576) | (39,355) | (22,155) | ||||

| Depreciation and amortization | (110,159) | (77,977) | (39,142) | (27,091) | ||||

| General and administrative expenses | (38,968) | (26,154) | (15,632) | (8,012) | ||||

| Development expenses | (8,373) | (7,892) | (2,904) | (3,350) | ||||

| Total operating expenses | (253,339) | (166,599) | (97,033) | (60,608) | ||||

| Gains (losses) from projects disposals | 96,431 | 611 | (1,397) | – | ||||

| Other income, net | 5,785 | 14,857 | 3,411 | 13,329 | ||||

| Operating profit | 278,781 | 143,561 | 70,038 | 65,792 | ||||

| Finance income | 36,292 | 18,299 | 28,126 | 3,234 | ||||

| Finance expenses | (136,457) | (85,836) | (54,171) | (36,525) | ||||

| Total finance expenses, net | (100,165) | (67,537) | (26,045) | (33,291) | ||||

| Profit before tax and equity loss | 178,616 | 76,024 | 43,993 | 32,501 | ||||

| Share of loss of equity accounted investees | (3,904) | (1,737) | (2,259) | (1,288) | ||||

| Profit before income taxes | 174,712 | 74,287 | 41,734 | 31,213 | ||||

| Taxes on income | (35,083) | (16,154) | (9,477) | (7,024) | ||||

| Profit for the period | 139,629 | 58,133 | 32,257 | 24,189 | ||||

| Profit for the period attributed to: | ||||||||

| Owners of the Company | 117,841 | 39,053 | 22,026 | 14,247 | ||||

| Non-controlling interests | 21,788 | 19,080 | 10,231 | 9,942 | ||||

| 139,629 | 58,133 | 32,257 | 24,189 | |||||

| Earnings per ordinary share (in USD) with a par value of NIS 0.1, attributable to owners of the parent Company: | ||||||||

| Basic earnings per share | 0.97 | 0.33 | 0.18 | 0.12 | ||||

| Diluted earnings per share | 0.91 | 0.32 | 0.16 | 0.12 | ||||

| Weighted average of share capital used in the calculation of earnings: | ||||||||

| Basic per share | 121,114,109 | 118,225,436 | 125,060,939 | 118,465,216 | ||||

| Diluted per share | 129,253,408 | 123,221,119 | 134,366,872 | 123,305,879 | ||||

(*) The Consolidated Statements of Income have been adjusted to present comparable information for the previous period. For additional details please see Appendix 9.

(**) Excluding depreciation and amortization.

| Consolidated Statements of Financial Position as of | ||||

| September 30 | December 31 | |||

| 2025 | 2024 | |||

| USD in | USD in | |||

| Thousands | Thousands | |||

| Assets | ||||

| Current assets | ||||

| Cash and cash equivalents | 679,827 | 387,427 | ||

| Deposits in banks | 1,409 | – | ||

| Restricted cash | 301,863 | 87,539 | ||

| Trade receivables | 86,627 | 50,692 | ||

| Other receivables | 72,932 | 99,651 | ||

| Other financial assets | 546 | 975 | ||

| Assets of disposal groups classified as held for sale | – | 81,661 | ||

| Total current assets | 1,143,204 | 707,945 | ||

| Non-current assets | ||||

| Restricted cash | 55,074 | 60,802 | ||

| Other long-term receivables | 64,184 | 61,045 | ||

| Deferred costs in respect of projects | 481,688 | 357,358 | ||

| Deferred borrowing costs | 1,262 | 276 | ||

| Loans to investee entities | 70,320 | 18,112 | ||

| Investments in equity accounted investees | 57,415 | – | ||

| Fixed assets, net | 5,243,053 | 3,699,192 | ||

| Intangible assets, net | 302,829 | 291,442 | ||

| Deferred taxes assets | 6,301 | 10,744 | ||

| Right-of-use asset, net | 222,420 | 210,941 | ||

| Financial assets at fair value through profit or loss | 83,644 | 69,216 | ||

| Other financial assets | 44,112 | 59,812 | ||

| Total non-current assets | 6,632,302 | 4,838,940 | ||

| Total assets | 7,775,506 | 5,546,885 | ||

| Consolidated Statements of Financial Position as of (Cont.) | ||||

| September 30 | December 31 | |||

| 2025 | 2024 | |||

| USD in | USD in | |||

| Thousands | Thousands | |||

| Liabilities and equity | ||||

| Current liabilities | ||||

| Credit and current maturities of loans from banks and other financial institutions | 751,015 | 212,246 | ||

| Trade payables | 130,009 | 161,991 | ||

| Other payables | 349,476 | 107,825 | ||

| Current maturities of debentures | 25,922 | 44,962 | ||

| Current maturities of lease liability | 11,386 | 10,240 | ||

| Other financial liabilities | 25,629 | 8,141 | ||

| Liabilities of disposal groups classified as held for sale | – | 46,635 | ||

| Total current liabilities | 1,293,437 | 592,040 | ||

| Non-current liabilities | ||||

| Debentures | 598,799 | 433,994 | ||

| Other financial liabilities | 211,300 | 107,865 | ||

| Convertible debentures | 264,052 | 133,056 | ||

| Loans from banks and other financial institutions | 2,556,884 | 1,996,137 | ||

| Loans from non-controlling interests | 86,192 | 75,598 | ||

| Financial liabilities through profit or loss | 26,688 | 25,844 | ||

| Deferred taxes liabilities | 67,998 | 41,792 | ||

| Employee benefits | 1,495 | 1,215 | ||

| Lease liability | 225,669 | 211,941 | ||

| Deferred income related to tax equity | 391,792 | 403,384 | ||

| Asset retirement obligation | 92,941 | 83,085 | ||

| Total non-current liabilities | 4,523,810 | 3,513,911 | ||

| Total liabilities | 5,817,247 | 4,105,951 | ||

| Equity | ||||

| Ordinary share capital | 3,693 | 3,308 | ||

| Share premium | 1,318,884 | 1,028,532 | ||

| Capital reserves | 79,917 | 25,273 | ||

| Proceeds on account of convertible options | 25,083 | 15,494 | ||

| Accumulated profit | 225,760 | 107,919 | ||

| Equity attributable to shareholders of the Company | 1,653,337 | 1,180,526 | ||

| Non-controlling interests | 304,922 | 260,408 | ||

| Total equity | 1,958,259 | 1,440,934 | ||

| Total liabilities and equity | 7,775,506 | 5,546,885 | ||

| Consolidated Statements of Cash Flows | |||||

| For the nine months ended September 30 | For the three months ended September 30 | ||||

| 2025 | 2024 | 2025 | 2024 | ||

| USD in | USD in | USD in | USD in | ||

| Thousands | Thousands | Thousands | Thousands | ||

| Cash flows for operating activities | |||||

| Profit for the period | 139,629 | 58,133 | 32,257 | 24,189 | |

| Income and expenses not associated with cash flows: | |||||

| Depreciation and amortization | 110,159 | 77,977 | 39,142 | 27,091 | |

| Finance expenses, net | 116,373 | 65,182 | 45,300 | 31,416 | |

| Share-based compensation | 5,047 | 6,027 | 2,053 | 1,942 | |

| Taxes on income | 35,083 | 16,154 | 9,477 | 7,024 | |

| Tax benefits | (62,059) | (10,102) | (23,087) | (3,576) | |

| Other income, net | (5,785) | (3,113) | (3,411) | (3,545) | |

| Company’s share in losses of investee partnerships | 3,904 | 1,737 | 2,259 | 1,288 | |

| Gains (losses) from projects disposals | (96,431) | (611) | 1,397 | – | |

| 106,291 | 153,251 | 73,130 | 61,640 | ||

| Changes in assets and liabilities items: | |||||

| Change in other receivables | (2,800) | 6,547 | 1,793 | 10,899 | |

| Change in trade receivables | (27,365) | (9,596) | (6,480) | (12,668) | |

| Change in other payables | 28,405 | (27) | 6,935 | (887) | |

| Change in trade payables | (5,418) | (941) | (2,768) | (85) | |

| (7,178) | (4,017) | (520) | (2,741) | ||

| Interest receipts | 9,921 | 7,805 | 3,587 | 2,439 | |

| Interest paid | (76,112) | (51,548) | (35,725) | (17,755) | |

| Income Tax paid | (10,093) | (6,084) | (1,420) | (1,301) | |

| Net cash from operating activities | 162,458 | 157,540 | 71,309 | 66,471 | |

| Cash flows for investing activities | |||||

| Sale (Acquisition) of consolidated entities, net | 37,832 | (1,849) | 4,814 | (461) | |

| Changes in restricted cash and bank deposits, net | (198,170) | (44,275) | (206,356) | (28,905) | |

| Purchase, development, and construction in respect of projects | (1,163,669) | (678,969) | (505,647) | (217,168) | |

| Loans provided and Investment in investees | (43,264) | (15,201) | (16,940) | (985) | |

| Repayment of loans to investees | 30,815 | 63 | – | 63 | |

| Loans provided to non-controlling interests | (297) | – | (297) | – | |

| Payments on account of acquisition of consolidated company | (7,447) | (15,697) | – | (4,846) | |

| Purchase of long-term financial assets measured at fair value through profit or loss, net | (5,257) | (12,204) | (2,010) | (864) | |

| Net cash used in investing activities | (1,349,457) | (768,132) | (726,436) | (253,166) | |

| Consolidated Statements of Cash Flows (Cont.) | |||||

| For the nine months ended September 30 | For the three months ended September 30 | ||||

| 2025 | 2024 | 2025 | 2024 | ||

| USD in | USD in | USD in | USD in | ||

| Thousands | Thousands | Thousands | Thousands | ||

| Cash flows from financing activities | |||||

| Receipt of loans from banks and other financial institutions | 1,324,524 | 667,857 | 649,840 | 337,408 | |

| Repayment of loans from banks and other financial institutions | (407,239) | (259,970) | (183,878) | (182,773) | |

| Issuance of debentures | 125,838 | – | – | – | |

| Issuance of convertible debentures | 114,685 | – | – | – | |

| Repayment of debentures | (47,545) | (26,016) | (25,551) | (24,732) | |

| Dividends and distributions by subsidiaries to non-controlling interests | (17,326) | (23,895) | (8,644) | (20,445) | |

| Proceeds from investments by tax-equity investors | 127,695 | 44,325 | 127,695 | 44,325 | |

| Repayment of tax-equity investment | (11,590) | – | (638) | – | |

| Deferred borrowing costs | (47,076) | (5,868) | (458) | (490) | |

| Repayment of loans from non-controlling interests | (858) | (2,017) | (858) | (1,017) | |

| Increase in holding rights of consolidated entity | (1,392) | (167) | – | – | |

| Receipt of loans from non-controlling interests | 182 | – | – | – | |

| Issuance of shares | 290,698 | – | 290,698 | – | |

| Exercise of share options | 45 | 14 | 15 | 1 | |

| Repayment of lease liability | (7,999) | (4,713) | (2,196) | (596) | |

| Proceeds from investment in entities by non-controlling interest | 12,799 | 179 | – | – | |

| Net cash from financing activities | 1,455,441 | 389,729 | 846,025 | 151,681 | |

| Increase (Decrease) in cash and cash equivalents | 268,442 | (220,863) | 190,898 | (35,014) | |

| Balance of cash and cash equivalents at beginning of period | 387,427 | 403,805 | 480,459 | 208,791 | |

| Effect of exchange rate fluctuations on cash and cash equivalents | 23,958 | (4,772) | 8,470 | 4,393 | |

| Cash and cash equivalents at end of period | 679,827 | 178,170 | 679,827 | 178,170 | |

Information related to Segmental Reporting

| For the nine months ended September 30, 2025 | ||||||||||||

| MENA | Europe | USA | Total reportable segments(**) | Others | Total | |||||||

| USD in thousands | ||||||||||||

| Revenues | 173,180 | 144,503 | 45,456 | 363,139 | 1,272 | 364,411 | ||||||

| Tax benefits | – | – | 65,493 | 65,493 | – | 65,493 | ||||||

| Total revenues and income | 173,180 | 144,503 | 110,949 | 428,632 | 1,272 | 429,904 | ||||||

| Segment adjusted EBITDA | 160,302 | 117,429 | 98,171 | 375,902 | 1,092 | 376,994 | ||||||

| Reconciliations of unallocated amounts: | ||||||||||||

| Headquarter costs (*) | (37,776 | ) | ||||||||||

| Intersegment profit | 172 | |||||||||||

| Gains from projects disposals | 54,597 | |||||||||||

| Depreciation and amortization and share-based compensation | (115,206 | ) | ||||||||||

| Operating profit | 278,781 | |||||||||||

| Finance income | 36,292 | |||||||||||

| Finance expenses | (136,457 | ) | ||||||||||

| Share in the losses of equity accounted investees | (3,904 | ) | ||||||||||

| Profit before income taxes | 174,712 | |||||||||||

(*) Including general and administrative and development expenses (excluding depreciation and amortization and share based compensation).

(**) Due to the Company’s organizational restructuring, the Chief Operation Decision Maker (CODM) now reviews the group’s results by segmenting them into three business units: MENA (Middle East and North Africa), Europe, and the US. Consequently, the Management and Construction segment has been excluded. The comparative figures for the nine-month and three-month periods ending September 30, 2024, have been updated accordingly.

Information related to Segmental Reporting

| For the nine months ended September 30, 2024 | ||||||||||||

| MENA | Europe | USA | Total reportable segments | Others | Total | |||||||

| USD in thousands | ||||||||||||

| Revenues | 121,607 | 147,164 | 8,611 | 277,382 | 7,208 | 284,590 | ||||||

| Tax benefits | – | – | 10,102 | 10,102 | – | 10,102 | ||||||

| Total revenues and income | 121,607 | 147,164 | 18,713 | 287,484 | 7,208 | 294,692 | ||||||

| Segment adjusted EBITDA | 99,659 | 129,386 | 15,965 | 245,010 | 3,858 | 248,868 | ||||||

| Reconciliations of unallocated amounts: | ||||||||||||

| Headquarter costs (*) | (25,108 | ) | ||||||||||

| Intersegment profit | 112 | |||||||||||

| Depreciation and amortization and share-based compensation | (84,004 | ) | ||||||||||

| Other incomes not attributed to segments | 3,693 | |||||||||||

| Operating profit | 143,561 | |||||||||||

| Finance income | 18,299 | |||||||||||

| Finance expenses | (85,836 | ) | ||||||||||

| Share in the losses of equity accounted investees | (1,737 | ) | ||||||||||

| Profit before income taxes | 74,287 | |||||||||||

(*) Including general and administrative and development expenses (excluding depreciation and amortization and share based compensation).

Information related to Segmental Reporting

| For the three months ended September 30, 2025 | ||||||||||||

| MENA | Europe | USA | Total reportable segments | Others | Total | |||||||

| USD in thousands | ||||||||||||

| Revenues | 77,543 | 45,319 | 15,448 | 138,310 | 226 | 138,536 | ||||||

| Tax benefits | – | – | 26,521 | 26,521 | – | 26,521 | ||||||

| Total revenues and income | 77,543 | 45,319 | 41,969 | 164,831 | 226 | 165,057 | ||||||

| Segment adjusted EBITDA | 53,271 | 35,203 | 38,258 | 126,732 | 13 | 126,745 | ||||||

| Reconciliations of unallocated amounts: | ||||||||||||

| Headquarter costs (*) | (14,818 | ) | ||||||||||

| Intersegment profit | 45 | |||||||||||

| Losses from projects disposals | (739 | ) | ||||||||||

| Depreciation and amortization and share-based compensation | (41,195 | ) | ||||||||||

| Operating profit | 70,038 | |||||||||||

| Finance income | 28,126 | |||||||||||

| Finance expenses | (54,171 | ) | ||||||||||

| Share in the losses of equity accounted investees | (2,259 | ) | ||||||||||

| Profit before income taxes | 41,734 | |||||||||||

(*) Including general and administrative and development expenses (excluding depreciation and amortization and share based compensation).

Information related to Segmental Reporting

| For the three months ended September 30, 2024 | ||||||||||||

| MENA | Europe | USA | Total reportable segments | Others | Total | |||||||

| USD in thousands | ||||||||||||

| Revenues | 55,566 | 46,041 | 5,180 | 106,787 | 2,708 | 109,495 | ||||||

| Tax benefits | – | – | 3,576 | 3,576 | – | 3,576 | ||||||

| Total revenues and income | 55,566 | 46,041 | 8,756 | 110,363 | 2,708 | 113,071 | ||||||

| Segment adjusted EBITDA | 44,786 | 46,133 | 8,134 | 99,053 | 1,567 | 100,620 | ||||||

| Reconciliations of unallocated amounts: | ||||||||||||

| Headquarter costs (*) | (9,479 | ) | ||||||||||

| Intersegment loss | (9 | ) | ||||||||||

| Depreciation and amortization and share-based compensation | (29,033 | ) | ||||||||||

| Other incomes not attributed to segments | 3,693 | |||||||||||

| Operating profit | 65,792 | |||||||||||

| Finance income | 3,234 | |||||||||||

| Finance expenses | (36,525 | ) | ||||||||||

| Share in the losses of equity accounted investees | (1,288 | ) | ||||||||||

| Profit before income taxes | 31,213 | |||||||||||

(*) Including general and administrative and development expenses (excluding depreciation and amortization and share based compensation).

Appendix 2 – Reconciliations between Net Income to Adjusted EBITDA

| ($ thousands) | For the nine months | For the three months | ||||||

| ended September 30 | ended September 30 | |||||||

| 2025 | 2024 | 2025 | 2024 | |||||

| Net Income | 139,629 | 58,133 | 32,257 | 24,189 | ||||

| Depreciation and amortization | 110,159 | 77,977 | 39,142 | 27,091 | ||||

| Share based compensation | 5,047 | 6,027 | 2,053 | 1,942 | ||||

| Finance income | (36,292) | (18,299) | (28,126) | (3,234) | ||||

| Finance expenses | 136,457 | 85,836 | 54,171 | 36,525 | ||||

| Gains from projects disposals (*) | (54,597) | – | 739 | – | ||||

| Non-recurring other income, net (**) | – | (3,693) | – | (3,693) | ||||

| Share of losses of equity accounted investees | 3,904 | 1,737 | 2,259 | 1,288 | ||||

| Taxes on income | 35,083 | 16,154 | 9,477 | 7,024 | ||||

| Adjusted EBITDA | 339,390 | 223,872 | 111,972 | 91,132 | ||||

| * Profit from revaluation linked to partial sale of asset. ** Recognition of income related to lower earn-out payments offset by a revaluation in the value of financial assets. | ||||||||

Appendix 3 – Debentures Covenants

Debentures Covenants

As of September 30, 2025, the Company was in compliance with all of its financial covenants under the indenture for the Series C, D, F, G and H Debentures, based on having achieved the following in its consolidated financial results:

Minimum equity

The company’s equity shall be maintained at no less than NIS 375 million so long as debentures F remain outstanding, NIS 1,250 million so long as debentures C and D remain outstanding, and USD 600 million so long as debentures G and H remain outstanding.

As of September 30, 2025, the company’s equity amounted to NIS 6,474 million (USD 1,958 million).

Net financial debt to net CAP

The ratio of standalone net financial debt to net CAP shall not exceed 70% for two consecutive financial periods so long as debentures F remain outstanding and shall not exceed 65% for two consecutive financial periods so long as debentures C, D, G and H remain outstanding.

As of September 30, 2025, the net financial debt to net CAP ratio, as defined above, stands at 34%.

Net financial debt to EBITDA

So long as debentures F remain outstanding, standalone financial debt shall not exceed NIS 10 million, and the consolidated financial debt to EBITDA ratio shall not exceed 18 for more than two consecutive financial periods.

For as long as debentures C and D remain outstanding, the consolidated financial debt to EBITDA ratio shall not exceed 15 for more than two consecutive financial periods.

For as long as debentures G and H remain outstanding, the consolidated financial debt to EBITDA ratio shall not exceed 17 for more than two consecutive financial periods.

As of September 30, 2025, the net financial debt to EBITDA ratio, as defined above, stands at 6.

Equity to balance sheet

The standalone equity to total balance sheet ratio shall be maintained at no less than 20% ,25% and 28%, respectively, for two consecutive financial periods for as long as debentures F, debentures C and D and debentures G and H remain outstanding.

As of September 30, 2025, the equity to balance sheet ratio, as defined above, stands at 58%.

A figure accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/804b52e2-c097-4b0a-b4ce-0e65a5ec9244

![]()